sevenstockstudio

Dwelling Depot (NYSE:HD) is a good firm with a easy and easy-to-understand enterprise mannequin. Our DCF fashions primarily based on Money Circulate Returns On Investments level to Dwelling Depot being undervalued by 25%. Share costs are down by 14% in comparison with the 52-week highs of $347, offering a compelling entry level for traders.

Dwelling Depot is the world’s largest dwelling enchancment retailer with over 2,300 shops throughout North America. Product ranges from constructing supplies, dwelling enchancment, backyard, décor, and upkeep and restore. Solely about 3.7% of revenues come from providers, which embody gear rental and residential enchancment set up. Their buyer teams are professionals and direct shoppers. Professionals are the renovators/remodelers, and the shoppers are the owners.

FY2023 and This autumn Monetary Overview

Contents

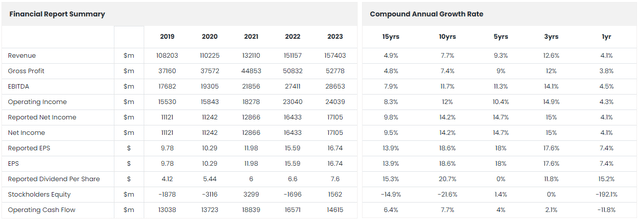

This autumn revenues had been roughly flat compared to the identical interval final 12 months. Margins remained secure and EPS was up 2.5% primarily because of the decrease shares excellent. Q3 noticed a rise in income of 6.5%, however This autumn noticed a slowdown. FY2023 (12 months ending January 2024) steering supplied by administration expects income development to be flat, working margins to go down from the present 15.3% to 14.5% and EPS to say no by round 5%. The margin decline is especially attributable to about $1bn additional pay for its frontline hourly staff.

FY2022 (12 months ending January 2023) noticed income development of 4.1%, margins noticed no change and EPS was 4.1% larger at $16.74.

Detailed Monetary Evaluation

For long-term worth creation, we have to see development, effectivity, and excessive returns. Just like a DuPont-like breakdown, we are going to try to establish the worth drivers for Dwelling Depot. We’ll have a look at the historic efficiency and the path the corporate is taking and use our understanding to mission ahead.

Monetary Abstract & Progress (ROCGA Analysis)

Allow us to begin by trying on the development numbers. 2021 noticed income improve from submit covid elevated demand in dwelling enchancment and from its acquisition of HD Provide. The three years CAGR in revenues of 12.6% are larger than the extra modest longer-term averages. As talked about above, FY2024 will see no development in revenues, and consensus expects development to start out choosing up once more in FY2025.

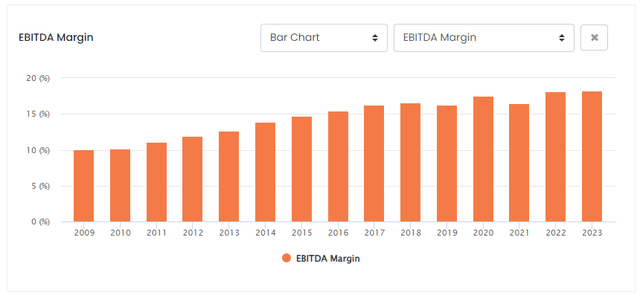

EBITDA Margins (ROCGA Analysis)

Margins have improved considerably from 2009’s 10% to 18.2% in 2023.

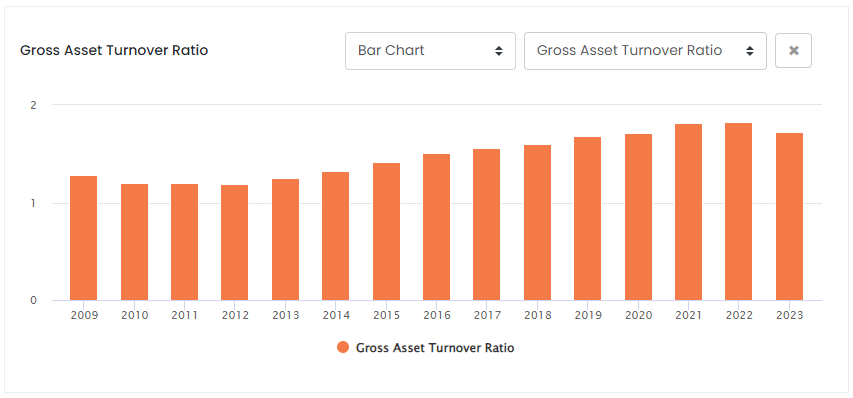

Gross Asset Turnover (ROCGA Analysis)

We are able to see that asset turnover has additionally improved over time. Asset turnover is calculated by dividing revenues by the property used to generate these property. Bettering asset turnover exhibits the corporate is healthier at utilizing its property to generate larger revenues.

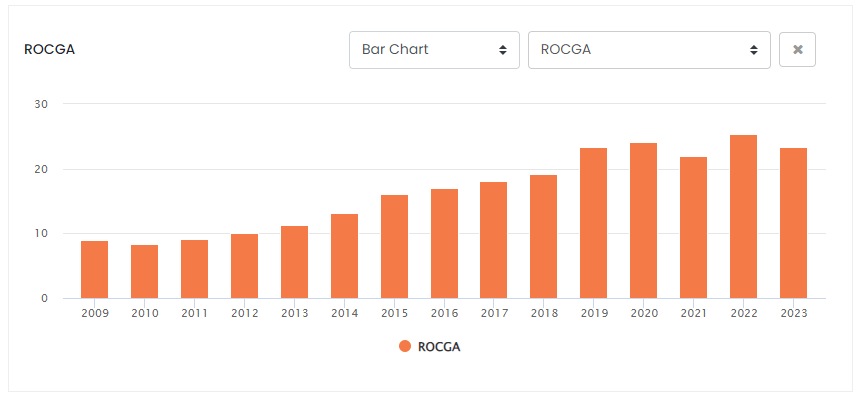

Returns On Money Producing Property (ROCGA Analysis)

Growing asset turnover and enhancing margins translate to enhancing returns. We are able to see within the chart above, returns have improved considerably over time and at the moment are standing properly above 20%. Returns On Money Producing Property (ROCGA) are just like Money Circulate Returns On Investments and are a measure of financial efficiency. So as to add worth, you want returns larger than the price of capital and development. Dwelling Depot suits all the factors required to be a serial worth creator.

Valuation

The share worth has greater than doubled from 2018’s low of $136 to the present share worth of $300. Even taking the excessive level at $207 per share, the share worth is up roughly 50%. The rise is much more spectacular if we return additional to 2013’s midpoint of roughly $56, the share worth has greater than quintupled (x5).

With the assistance of our money movement returns on Investments primarily based DCF valuation device, we are going to use the info gathered to this point to derive an intrinsic worth for Dwelling Depot. The valuation device provides us the flexibility to back-test our mannequin assumptions and use that to mission ahead.

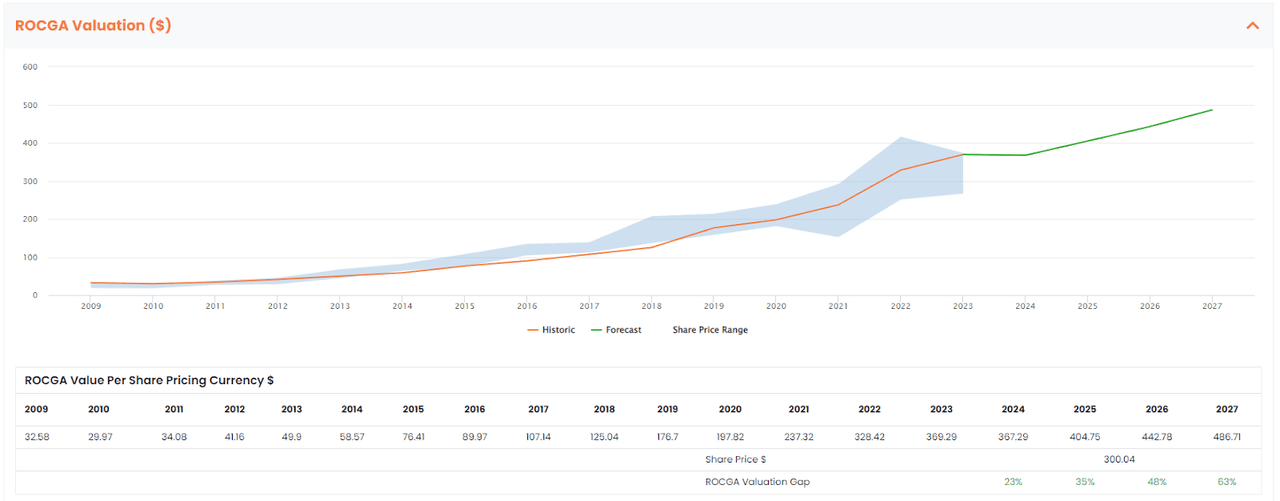

HD Default Valuation chart (Created by the writer utilizing ROCGA Analysis platform)

The valuation chart above exhibits the historic share worth highs and lows (the blue band) and the model-driven valuation, the orange line. The valuation line follows carefully with the share worth band and that offers us the arrogance to make use of the identical mannequin to mission ahead. The inexperienced line is the valuation forecast derived from our default back-tested mannequin and consensus earnings estimates.

This Money Circulate Returns On Investments primarily based DCF valuation device factors to Dwelling Depot being undervalued by at the very least 23%. Being in step with its historical past of making worth, valuation is predicted to proceed growing for FY2025 and past.

High quality & Dangers

The dividend yield is a good 2.6% with the quilt hovering round and over 2x.

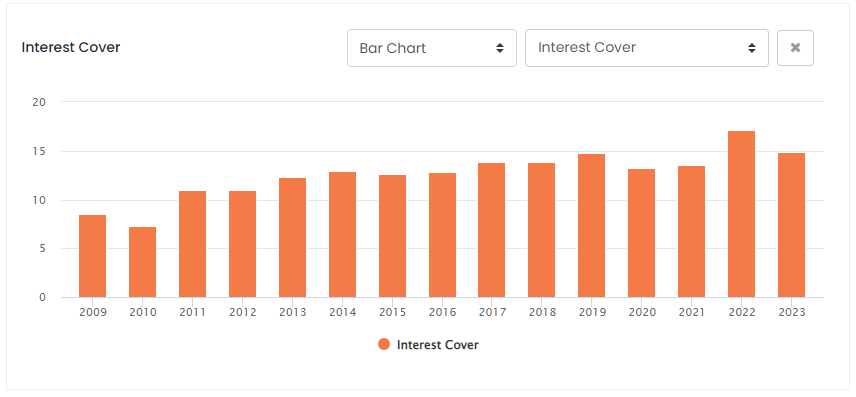

Curiosity Cowl (ROCGA Analysis)

Curiosity cowl can be sturdy within the mid-teens. EPS has grown by 13.9% over the previous 15 years. All the above indicators are of fine monetary high quality. The corporate additionally has a prolific share buyback program. The present shares excellent are roughly 1,013m, down a 3rd from 2013’s 1,499m, returning over $70bn within the course of. Financially, the corporate is secure and powerful.

2022 noticed a build-up in stock from $16.6bn to $22.1bn, and this stood at $24.9bn on the 12 months ending January 2023.

Working capital was impacted by larger merchandise inventories ensuing from our efforts to proceed to satisfy the demand surroundings and from larger product and transportation prices, together with the timing of vendor funds.

It might seem that the buildup of stock occurred when income development was excessive, however with slowing development weren’t in a position to promote rapidly sufficient. This had a destructive impact on money flows. The corporate may very well be holding onto some probably redundant inventory (destructive), and these are at decrease pre-high inflation costs (optimistic). With the income development anticipated to be flat subsequent 12 months, we should always anticipate the unwinding of this working capital and better working money flows.

Given the macroeconomic backdrop, administration expects flat actual financial development and shopper spending in 2023. That is additionally evident within the income development expectations. One other level price mentioning is that Dwelling Depot has virtually overwhelmingly had optimistic earnings and income surprises, so the chance on that’s to the upside.

The inflationary surroundings will influence Dwelling Depot. Flat development in an inflationary surroundings does imply a modest discount in precise development. Wage inflation is already having an influence on margins.

Greater mortgage prices will preserve individuals of their houses for longer and should encourage restore, renovation, and transforming.

Conclusion

Dwelling Depot has demonstrated its means as a serial worth creator, has sturdy fundamentals, and given the present share worth, is presenting a reduction of over 20%. They are going to proceed so as to add worth past 2024.

Lowe’s, compared, is trying extra enticing on numerous valuation matrices. On condition that revenues are anticipated to say no by roughly 8%, Dwelling Depot appears higher positioned as to if the upper inflation, decrease development surroundings.

It’s a good time to go lengthy Dwelling Depot inventory.